SCSS Scheme in Post Office, An increase of Rs 15 lakhs to Rs 30 lakhs has been made to the maximum contribution amount under the senior citizen savings plan. The monthly savings initiative has increased its maximum deposit limit from Rs 4.5 lakh to Rs 9 lakh for a single account and from Rs 9 lakh to Rs 15 lakh for a combined account.

Contents

डाकघर निवेश-बचत योजनाएं

डाकघर बचत योजनाएं जोखिम रहित निवेश पुरस्कार और कई भरोसेमंद वस्तुएं प्रदान करती हैं। देश भर में लगभग 1.54 लाख डाकघर ये कार्यक्रम चलाते हैं। उदाहरण के लिए, प्रत्येक शहर में 8200 सार्वजनिक क्षेत्र के बैंकों और डाकघरों के माध्यम से, सरकार पीपीएफ कार्यक्रम चलाती है। चूंकि वे सरकार द्वारा समर्थित हैं, इसलिए इन निवेशों पर गारंटीकृत रिटर्न मिलता है। डाकघर की योजनाओं में निवेश लक्ष्य प्राप्ति और आपातकालीन जरूरतों के लिए एक कोष बनाने में योगदान देता है। इसके अतिरिक्त, वे आयकर अधिनियम की धारा 80 सी के तहत 1.5 लाख रुपये तक के कर लाभ प्रदान करते हैं। डाकघर के कई कार्यक्रमों को यहाँ विस्तार से बताया गया है।

Also Read: PM Awas Yojana List, digitizeindiagovin.com, Typingspeedtestonline, Nebsit Council

Comparison of Interest Rates of Various Post Office Savings Schemes

| Scheme | Interest Rate (Applicable from 01/04/2024) | Minimum Investment | Maximum Investment | Eligibility | Tax Implications |

| Post Office Savings Account | 4% per annum (p.a.) | Rs. 500 | No limit | Resident Indian, minor(above 10 years) and major | Tax-free interest up to Rs 50,000 for senior citizens |

| Post Office Time Deposit Account (TD) | One-year – 6.9% p.a. Two-year – 7.0% p.a. Three-year – 7.1% p.a. Five-year – 7.5% p.a. (Compounded Quarterly) | Rs 1,000 | No limit | Resident Indian, minor(above 10 years) and major | -Tax benefits available under Section 80C only if the deposit is held for 5 years. -Interest earned is taxable -TDS to be deducted on interest earned for more than Rs 40,000 p.a.(Rs 50,000 in case of senior citizens) |

| Post Office Monthly Income Scheme Account (MIS) | 7.4% per annum payable monthly | Rs 1,000 | For a single account- Rs 9 lakh Joint account accounts- Rs 15 lakh | Resident Indian, minor(above 10 years) and major | – Tax benefit under Section 80C for deposits –Interest earned is taxable -TDS to be deducted on interest earned for more than Rs 50,000 p.a. |

SCSS Scheme in Post Office

| enior Citizen Savings Scheme (SCSS) | 8.2% p.a. (Compounded Quarterly) | Rs 1,000 | Maximum deposit over the lifetime allowed at Rs 30 lakh | Individuals of age> 60 years or age between 55 and 60 for retired civilian or defense employees | – Tax benefit under Section 80C for deposits – TDS to be deducted on interest earned for more than Rs 50,000 p.a. |

| 15-year Public Provident Fund Account (PPF) | 7.1% p.a. (Compounded annually) | Rs 500 per financial year | Rs 1.5 lakh per financial year | Resident Indian, minor and major | Tax rebate under Section 80C for deposits (maximum Rs 1.5 lakh p.a.) interest is tax-free. |

| National Savings Certificates (NSC) | 7.7% p.a. (Compounded annually) | Rs 1,000 | No limit | Resident Indian, minor and major | Tax rebate under section 80C for deposits (maximum Rs 1.5 lakh p.a.) |

| Kisan Vikas Patra (KVP) | 7.5% p.a. (Compounded annually) | Rs 1,000 | No limit | Resident Indian, minor and major | Interest is taxable, but no tax on the amount received on maturity |

| Sukanya Samriddhi Accounts | 8.2% p.a. (Compounded annually) | Rs 250 per financial year | Rs 1.5 lakh per financial year | Girl Child – up to 10 years from birth | Investment (up to Rs 1.5 lakh exempt under Section 80C), interest and amount received on maturity is tax-free |

Savings Schemes Under Post Office Investments

Post Office Savings Account

- To start a post office savings account, you need to deposit at least Rs 500.

- The domestic client has the option of opening an account under sole or joint ownership.

- The deposits made into the post office account are subject to an interest rate of 4% per year.

- On request, you can use the account to access a chequebook, ATM card, online and mobile banking, and other services. Every fiscal year ends with interest being credited.

- Under Section 80TTA of the Income Tax Act, an individual may deduct up to Rs 10,000 from their entire income.

- When funds are not added to or removed from an account for three consecutive fiscal years, the account is considered silent or dormant.

- Reactivation of such an account is possible by submitting an application to the relevant Post Office together with current KYC documentation and a passbook.

5-वर्षीय डाकघर आवर्ती जमा खाता (आरडी)

- जैसा कि नाम से ही स्पष्ट है, इस आरडी खाते की अवधि पांच वर्ष निर्धारित की गई है।

- आप 100 रुपये या उससे अधिक की निश्चित मासिक जमा राशि पर 6.7% प्रति वर्ष की दर से ब्याज का भुगतान करना चुन सकते हैं।

- प्रत्येक तिमाही में, ब्याज चक्रवृद्धि होता है।

- एक बार 12 किस्तों का समय पर और बिना चूक के भुगतान करने पर, आप खाते में उपलब्ध जमा राशि के विरुद्ध 50% तक का ऋण प्राप्त कर सकते हैं।

- संबंधित डाकघर में आवेदन करके खाते का पांच साल का विस्तार प्राप्त किया जा सकता है। खाता पहली बार खोले जाने पर जो ब्याज दर लागू थी, वह विस्तार के दौरान लागू होगी।

- खाता खोलने की तिथि से तीन वर्ष के बाद, संबंधित डाकघर को आवश्यक आवेदन पत्र भेजकर आरडी खाते को समय से पहले रद्द किया जा सकता है।

- यदि पीओ बचत खाता समय से पहले ही बंद कर दिया जाता है, यहां तक कि परिपक्व होने से एक दिन पहले भी, तो ब्याज दर वसूली जाएगी।

Also Read: Kusum Solar Yojana Maharashtra, Mobilenumbertrackeronline, indnewsupdates.com, ssorajasthanidlogin.com,

Post Office Time Deposit Account (TD)

- Post office time deposit accounts are available in four different tenures: one year, two years, three years, and five years.

- This account allows a minimum deposit of Rs 1,000.

- Although it is payable annually, the interest is computed on a quarterly basis. The following interest rates apply to Q2 FY 2024–2025, which runs from July 1 to September 30, 2024:

| Period | Rate of Interest |

| 1-year account | 6.9% |

| 2 year account | 7% |

| 3-year account | 7.1% |

| 5 year account | 7.5% |

- The investment in the five-year-term account is eligible for a deduction under Section 80C.

- You may also use this Post Office TD account as collateral for loans from scheduled or cooperative banks, RBI, home financing companies, government agencies, and other entities by completing the applicable application at the Post Office and providing proof of acceptance in the form of an acknowledgement letter from the recipient.

- It is not possible to withdraw deposits prior to the six-month period that starts on the deposit date.

- Premature closure of TD accounts is possible by sending an application form along with the passbook to the relevant post office.

- The PO Savings Account Interest Rate will be applied to any TD account cancellations made during the first year but prior to the end of six months.

Post Office Monthly Income Scheme Account (MIS)

- A single account can accept deposits up to Rs 9 lakh, while a joint account can accept deposits up to Rs 15 lakh.

- During Q2 FY 2024–2025, you can earn an interest rate of 7.4% p.a. through this account and receive a fixed monthly income from the scheme.

- Five years is the maturity period for POMIS.

- Account closure and money return to the nominee are possible outcomes if the account holder passes away before the account matures. The money is refunded once the prior month’s interest has been paid. Account closure and money return to the nominee are possible outcomes if the account holder passes away before the account matures. A refund occurs once the interest from the prior month is paid off.

- There will be a deduction of 2% of the principal amount if the account is closed within the first year but before the third year from the date of opening. It will be settled for the remaining amount.

- If the account is closed after three years but five years from the date of opening, there will be a one per cent decrease from the principle amount. The outstanding amount will be settled.

- Premature account closure is possible by bringing the passbook and the required application form to the relevant Post Office. The account cannot be prematurely closed before its full year has passed. If a closure is made earlier than a year, there may be consequences.

SCSS Scheme in Post Office

- For instance, you will receive interest of Rs 5,325 per month until the end of the term if you invest up to the maximum of Rs 9 lakh in a Post Office MIS account for a period of five years. After the five years are up, you will receive the Rs 9 lakh deposit back.

- While interest from post office MIS is paid on a monthly basis during the scheme’s duration, interest income from post office TD/RD is earned at the conclusion of the period.

वरिष्ठ नागरिक बचत योजना (एससीएसएस)

- सरकार द्वारा समर्थित SCSS सेवानिवृत्ति कार्यक्रम के साथ, आप किसी भी समय पूरा या सिर्फ़ एक किस्त में योगदान कर सकते हैं।

- जमा राशि 1,000 रुपये से लेकर 30 लाख रुपये तक हो सकती है।

- केवल एक पति या पत्नी ही अलग-अलग या संयुक्त रूप से खाता खोल सकते हैं।

- वित्त वर्ष 2024-2025 की दूसरी तिमाही के लिए, योजना में 8.2% प्रति वर्ष की ब्याज दर प्रस्तावित है। ब्याज का भुगतान तिमाही आधार पर किया जाना चाहिए।

- यह खाता 60 वर्ष से अधिक आयु का कोई भी व्यक्ति खोल सकता है।

- खाता खोलने की सुविधा सेवानिवृत्त सैन्य कर्मियों और नागरिक कर्मचारियों के लिए भी उपलब्ध है, जिनकी आयु 50 से 60 वर्ष के बीच है। हालांकि, उन्हें अपने सेवानिवृत्ति लाभों को प्राप्त करने के एक महीने के भीतर निवेश करना होगा।

- आयकर अधिनियम की धारा 80C इस योजना के तहत किए गए निवेश पर कटौती की अनुमति देती है।

How to Open a Post Office Saving Schemes Account?

Post Office Savings Plans are appropriate for people who don’t want to take on too much risk. These schemes are perfect for risk-averse investors who nonetheless want to maximise their savings because their rewards are not subject to market swings. A post office savings scheme account can be opened online using Internet banking, a mobile app, or by downloading the application for opening an account.

Also Read: PM Pranam Yojana, shaladarpanportalgov.com, yojanaforall.com, Onlinereferjobs

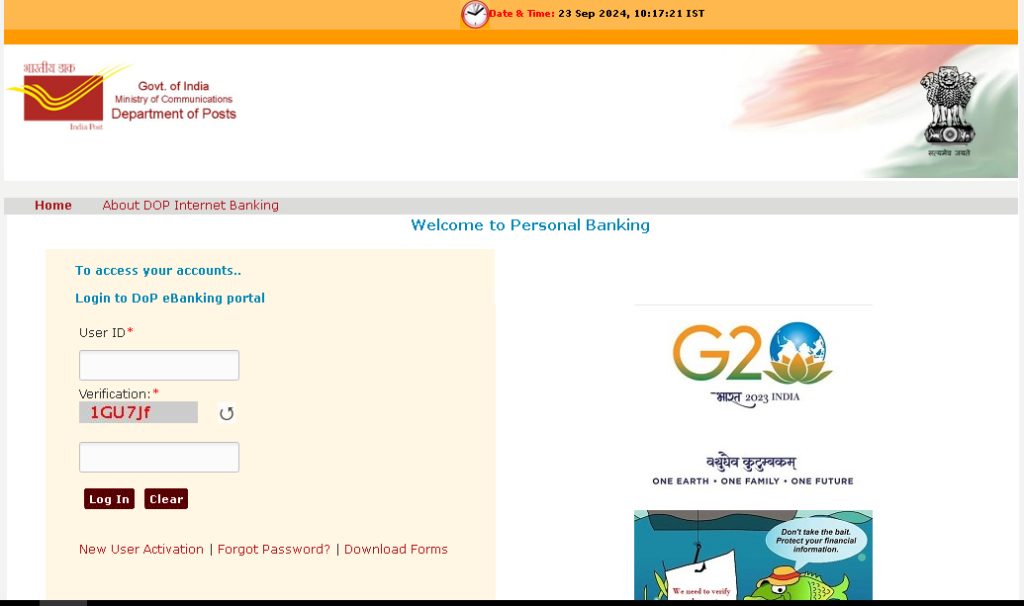

Through Internet Banking

- First, go to the Department of Posts (DOP) online banking page.

- Step 2: Press the option labelled New User Activation.

- Step 3: After entering the Account ID and Customer ID, click Continue. If you would like to activate Internet banking, you can also go to the post office branch in your home, complete the application, and provide the necessary paperwork.

- Step 4: To access your DOP online banking when Internet banking has been enabled, enter your user ID and password.

- Step 5: Select the Service Request tab from the menu after selecting the ‘General Service’ tab.

- Step 6: Select the ‘New Requests’ tab from the ‘Service Request’ section.

- Step 7: From the list of possibilities, choose the account type you wish to open.

- Step 8: Fill out the application form with the necessary information, then click Submit.

Faq’s

Q. Does investing in post office savings schemes result in a tax rebate?

Ans: For investments made in the majority of post office savings plans, you are eligible for the Section 80C deduction. Recurring deposit plans and investment post office MIS are not eligible for this type of tax deduction, nevertheless.

Q. Can students start a savings account at the post office?

Ans: Yes, investors in the Post Office Savings Scheme may be students over the age of eighteen. The Senior Citizen Savings Scheme (SCSS), which can only be opened by females under the age of ten, and the Sukanya Samriddhi Yojana (SSY), which can only be opened by senior citizens, are the only post office savings plans that students are not allowed to open.

@PAY