Contents [show]

Atal Pension Yojana, Atal pension scheme, APY chart, Atal pension yojana form Atal Pension Yojana Scheme Benefits

Atal pension yojana is a pension scheme which is focused to provide benefits to the unorganized sector of India. Atal Pension Yojana is the pension scheme of Government of Indian launched in the year 2015 by the Prime Minister of India.

Under Atal Pension scheme, a guaranteed minimum monthly pension of Rs.1000/-, Rs.2000/-, Rs.3000/-, Rs.4000/- and Rs.5000/- will be provided to the subscribers on the basis of the contribution made by them. Atal Pension is launched with an aim to provide retirement benefits to the workers in the unorganized sectors. On contributing to this scheme, they can save their retirement. Pension Fund Regulatory and Development Authority (PFRDA) is the government body that administers the APY under the National Pension Scheme Architecture. The investment guidelines for this scheme are prescribed by the Ministry of Finance, Government of India. AYP is basically a Social Security Scheme that was launched as a replacement to a pre-existing Swavalamban Yojana. APY scheme is open to all the bank accounts.

Name of the scheme Atal Pension Yojna (APY) Article category Information Administered by Pension Fund Regulatory and Development Authority (PFRDA) Population covered Unorganized sector Launch year 2015 Status Active Atal Pension Yojana Eligibility

In order to become the subscriber of Atal Pension Yojana, one must fulfill the eligibility criteria-

Subscriber should be an Indian citizen. Prospective applicants must have age between 18 years to 40 years. He/she should have a saving bank account or have to open a bank account. Applicants should have a valid mobile no. and all its details should be furnished to the bank at the time of registration.

Benefits of APY

The pension is guaranteed by the Government of India. Subscriber of APY gets a guaranteed pension of Rs.1000/- to Rs.5000/- per month. Under this scheme, subscribers can also increase or decrease the pension amount once a year, during the accumulation phase. The scheme is not only beneficial for the subscriber, but also for his/her spouse. In case of death of the subscriber, the spouse will be entitled to the pension. In case of demise of both subscriber and spouse, the nominee will be entitled to get the same pension. The tax benefits under this scheme are the same as applicable under NPS (National Payment Scheme). APY is also beneficial as the government also co-contribute Rs.1000/- per year or 50% of the total contribution whichever is low. The beneficiary of any statutory social security schemes are not eligible to receive the benefit of Government co-contribution under APY. Below, we have shared some of the enactments for which government’s co-coordination is not provided-

Employees’ Provident Fund & Miscellaneous Provision Act, 1952. The Coal Mines Provident Fund and Miscellaneous Provision Act, 1948. Seamen’s’ Provident Fund Act, 1966. Assam Tea Plantation Provident Fund and Miscellaneous Provision, 1955. Jammu Kashmir Employees’ Provident Fund & Miscellaneous Provision Act, 1961. Any other statutory social security scheme.

APY Features

- Guaranteed monthly pension for subscribers, ranging from Rs. 1,000 to Rs. 5,000 per month.

- Government of India (GoI) will also co-contribute 50% of the subscriber’s contribution or Rs. 1,000 per annum, whichever is lower. The Government co-contribution is available for those who are not covered by any Statutory Social Security Schemes and is not an Income Taxpayer

- GoI will co-contribute to each eligible subscriber, for a period of 5 years who joins the scheme in the period June 1 to December 31, 2015. The benefit of five years of Government co-contribution under APY would not exceed 5 years for all subscribers including migrated Swavalamban beneficiaries.

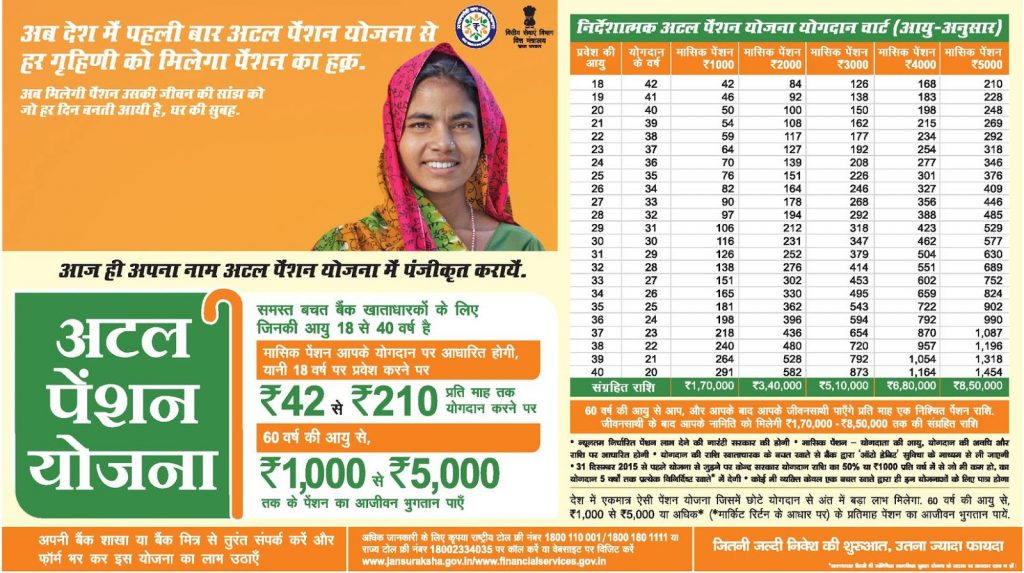

Indicative APY Contribution Chart (Age wise)

| Age of Entry | Years of Contribution | Monthly pension of Rs. 1000. | Monthly pension of Rs. 2000. | Monthly pension of Rs. 3000. | Monthly pension of Rs. 4000. | Monthly pension of Rs. 5000. |

|---|---|---|---|---|---|---|

| 18 | 42 | 42 | 84 | 126 | 168 | 210 |

| 19 | 41 | 46 | 92 | 138 | 183 | 228 |

| 20 | 40 | 50 | 100 | 150 | 198 | 248 |

| 21 | 39 | 54 | 108 | 162 | 215 | 269 |

| 22 | 38 | 59 | 117 | 177 | 234 | 292 |

| 23 | 37 | 64 | 127 | 192 | 254 | 318 |

| 24 | 36 | 70 | 139 | 208 | 277 | 346 |

| 25 | 35 | 76 | 151 | 226 | 301 | 376 |

| 26 | 34 | 82 | 164 | 246 | 327 | 409 |

| 27 | 33 | 90 | 178 | 268 | 356 | 446 |

| 28 | 32 | 97 | 194 | 292 | 388 | 485 |

| 29 | 31 | 106 | 212 | 318 | 423 | 529 |

| 30 | 30 | 116 | 231 | 347 | 462 | 577 |

| 31 | 29 | 126 | 252 | 379 | 504 | 630 |

| 32 | 28 | 138 | 276 | 414 | 551 | 689 |

| 33 | 27 | 151 | 302 | 453 | 602 | 752 |

| 34 | 26 | 165 | 330 | 495 | 659 | 824 |

| 35 | 25 | 181 | 362 | 543 | 722 | 902 |

| 36 | 24 | 198 | 396 | 594 | 792 | 990 |

| 37 | 23 | 218 | 436 | 654 | 870 | 1,087 |

| 38 | 22 | 240 | 480 | 720 | 957 | 1,196 |

| 39 | 21 | 264 | 528 | 792 | 1,054 | 1,318 |

Atal Pension Yojana, Atal pension scheme, APY chart, Atal pension yojana form

How to apply for Atal Pension Yojana Online

To enroll for Atal Pension Yojna (APY) account, the applicant has to follows an easy procedure. The step-by-step guide is given below-

- Approach the bank branch where the applicant’s savings account is held. In case of the applicant have not an account he/she can open one.

- Fill the APY application form. Provide an Aadhar card/ mobile number.

- Complete all the other formalities.

- Once the account is opened, the subscriber must ensure that there is a minimum required balance in the account for the transfer monthly contribution for this scheme.

- Apart from this, applicants can also fill the APY registration form and enroll them by using net banking.

- The subscriber can open an only account under his/her name.

- At the time of application, it is mandatory for subscribers to furnish the details of the nominee wherever applicable in APY account.

- They also have to provide their Aadhaar details.

- After successful enrolment, periodic statements will be provided to the subscribers as part of intimation.

- Subscriber will receive statements of account in the form of SMS alert as well as in physical form.

[signinlocker id=”221″] [/signinlocker]

For complete Scheme Detail & form please click the link

APY account can be withdrawn in the following conditions

Subscriber attains the age of 60 years Subscriber can exit from APY on the completion of 60 years. After that pension will be made available to the subscriber with 100% annuitization.

Death of subscriber In case of death of the subscriber, the return of corpus () will be made available to the spouse. And if both subscribers dies, the pension amount will be given to the nominee.

Exit before the age of 60 years The early exit before the age of 60 years is not permitted. However, it is permitted only in exceptional circumstances such as the death of terminal disease or death of the subscriber/ beneficiary. Atal Pension Yojana Penalty for Default

The saving account under APY will be considered default if sufficient balance will not be maintained for contribution on the due date. In such a situation, the bank will charge an extra amount for delayed payments.

The additional amount that will be collected from the account holder is shared below-

One rupee per month for the contribution up to Rs.100/- per month. Two rupees per month for contribution between Rs.101 to 500/- per month. Five rupees per month for the contribution of Rs.501/- to Rs.1000/- per month. Rs.10/- per month for contribution more than Rs.1001/- per month.

Atal Pension Scheme Discontinuation of payment

Subscribers must ensure that their APY account is funded enough for auto-debit of contribution amount. Otherwise, subscribers will face the following issues if there is a discontinuation of payments of contribution amount-

After 6 months, APY account will freeze After 12 months, APY account will be deactivated after 12 months, APY account will be closed Swavalamban Yojana and Atal Pension Yojana

Atal Pension Yojana is a replacement of Swavalamban Yojna with additional features. The registered users/ subscriber of Swavalamban Yojna aged between 18 -40 years were migrated to APY scheme. However, it was all upon the subscribers (of age beyond 40 years) whether they want to opt-out the Swavalamban Scheme with the withdrawal of lump-sum amount or to continue till the age of 60 years.

Also Read: Apply for Apna CSC online Digital Seva Registration 2019

Fill the APY application form. Provide an Aadhar card/ mobile number. Complete all the other formalities. Once the account is opened, the subscriber must ensure that there is a minimum required balance in the account for the transfer monthly contribution for this scheme. Apart from this, applicants can also fill the APY registration form and enroll them by using net banking. The subscriber can open an only account under his/her name. At the time of application, it is mandatory for subscribers to furnish the details of the nominee wherever applicable in APY account. They also have to provide their Aadhaar details.

After successful enrolment, periodic statements will be provided to the subscribers as part of intimation. Subscriber will receive statements of account in the form of SMS alert as well as in physical form. APY account can be withdrawn in the following conditions-

Subscriber attains the age of 60 years Subscriber can exit from APY on the completion of 60 years. After that pension will be made available to the subscriber with 100% annuitization.

Death of subscriber In case of death of the subscriber, the return of corpus () will be made available to the spouse. And if both subscribers dies, the pension amount will be given to the nominee.

Exit before the age of 60 years The early exit before the age of 60 years is not permitted. However, it is permitted only in exceptional circumstances such as the death of terminal disease or death of the subscriber/ beneficiary. Atal Pension Yojana Penalty for Default

The saving account under APY will be considered default if sufficient balance will not be maintained for contribution on the due date. In such a situation, the bank will charge an extra amount for delayed payments.

The additional amount that will be collected from the account holder is shared below-

One rupee per month for the contribution up to Rs.100/- per month. Two rupees per month for contribution between Rs.101 to 500/- per month. Five rupees per month for the contribution of Rs.501/- to Rs.1000/- per month. Rs.10/- per month for contribution more than Rs.1001/- per month.

Atal Pension Scheme Discontinuation of payment

Subscribers must ensure that their APY account is funded enough for auto-debit of contribution amount. Otherwise, subscribers will face the following issues if there is a discontinuation of payments of contribution amount-

After 6 months, APY account will freeze After 12 months, APY account will be deactivated after 12 months, APY account will be closed Swavalamban Yojana and Atal Pension Yojana

Atal Pension Yojana is a replacement of Swavalamban Yojna with additional features. The registered users/ subscriber of Swavalamban Yojna aged between 18 -40 years were migrated to APY scheme. However, it was all upon the subscribers (of age beyond 40 years) whether they want to opt-out the Swavalamban Scheme with the withdrawal of lump-sum amount or to continue till the age of 60 years.

Also Read: Digitize India Registration On digitizeindia.gov.in | Sign Up For Data Entry Job

Ques.- What are the minimum and maximum age of joining Atal Pension Scheme?

Ans.- The minimum age of joining APY is 18 years whereas the maximum age is 20 years.

Ques.- How subscriber will know the status of the contribution?

Ans.- The status will be intimated to the subscriber through SMS alerts on their registered mobile no. Apart from this, subscribers will also receive a physical statement of Account.

Ques.- In case of change of residence/shifting from the city, how can subscriber make a contribution to APY?

Ans.- In the case of a dislocation, a contribution can be remitted through the auto-debit facility.

Ques.- Is it compulsory to have a saving bank account for joining AYP?

Ans.- Yes, it is mandatory for subscribers to have a saving bank account to join APY scheme.

Ques.- What is the due date for monthly contribution?

Ans.- The due date is decided according to the initial date of deposit of contribution to APY account.

Ques.- How co-coordination does Government provide into this scheme?

Ans.- Government of India provide co-contribution of 50% to the contribution of the subscriber or Rs.1000/- per annum, whichever is lower. This co-contribution is only provided to those who are not tax-payer or beneficiary of any Statutory Social Security Scheme.

Co-contribution is eligible to each APY subscriber for 5 years who enroll in the scheme between 1st June 2015 to 31st December 2015. The benefit of co-contribution is only for five years for all the subscribers include subscribers of Swavalamban Scheme.

Pingback: Mobile Number Tracker - Mobile Number Tracker